Canadian inflation is officially “too high,” putting the Bank of Canada’s (BoC) credibility into jeopardy for the second time in five years. April inflation data breached the central bank’s upper tolerance band—just weeks after it dismissed accelerating price growth and cut rates, effectively adding inflationary stimulus. BMO had a blunt warning to investors this week: Another cut at these levels would force markets to doubt the BoC’s commitment to its sole mandate: inflation control.

Canadian Inflation Headline Data Temporarily Lowered By Carbon Tax

Headline CPI fell sharply to 1.7% in April (from 2.3% in March), artificially lowered by the carbon tax removal. This abruptly lowered energy prices such as gasoline (-10.2%), natural gas (-18.9%), and heating oil (-8.4%).

“The carbon tax had been building over most of the past decade and was removed in one fell swoop, creating an outsized shock,” explains Benjamin Reitzes, BMO’s Rate & Marco Strategist. “Unfortunately, excluding energy, inflation wasn’t nearly as friendly.”

BoC-Preferred Inflation Data Smashes Above Tolerance Range

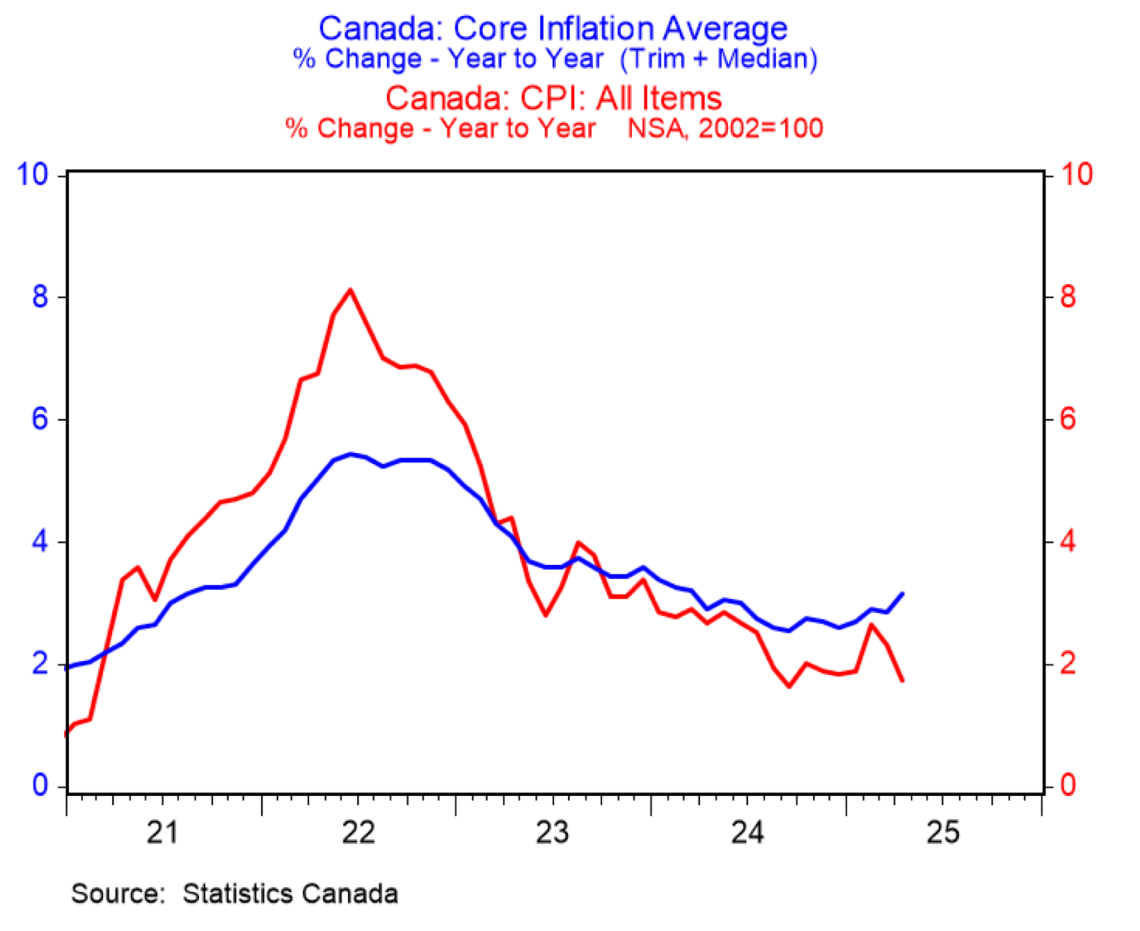

Central banks with an inflation mandate are looking to manage currency erosion (a.k.a. inflation). One time shocks due to abrupt policy shifts aren’t a matter of monetary policy, they’re largely seen as temporary noise. As a result, they rely on CPI-Core measures that eliminate the most volatile movements from the inflation basket, instead of using the headline data we’re all discussing.

The bank notes that simply stripping out energy pushes CPI to 2.9%, the highest rate in a year. CPI-Core is even higher.

“Similarly, the Bank of Canada’s core inflation metrics also hit one-year highs of above 3%. That’s a long way from the Bank’s 2% inflation target, which has been elusive since 2021,” explains Reitzes.

The central bank’s inflation target is 2%, but it considers up to 3% to be a tolerable level. As it inches towards the upper bound of tolerance, the Bank of Canada (BoC) typically begins moving towards slowing inflation. They did the exact opposite when it made its last cut, helping to push CPI-Core (3.1%) above and out of its tolerance band.

BoC Commitment To Mandate Questionable If It Cuts Rates w/High Inflation

Until this week, most experts anticipated the BoC would slash rates at its June announcement. Since then, the odds of a rate cut have plunged to 40%, but that’s still relatively high. Expectations of a rate cut persist despite elevated inflation.

“Some of the details on inflation breadth weren’t as troubling, but cutting in the face of 3% core inflation is questionable,” explains Reitzes.

There’s still a few major indicators that may provide warning signs for the BoC. In its recent reports they’ve attempted to forecast where inflation is heading based on major indicators like employment and GDP. However, they’ve been largely unsuccessful, tending to underestimate the resilience of the Canadian economy.

“We still have Q1 GDP and the flash estimate for April GDP, but it’s going to be challenging for the Bank to cut again in June as things stand without facing serious criticism about the seriousness of its mandate,” warns Reitzes.

Canadians would have a much bigger problem than a few extra basis points on loans or elevated inflation if this happens. A currency is only as strong as the issuer, and its commitment to defend the paper it backs. Failing to meet self-created targets twice under a single governor is the kind of thing that can destroy decades of hard-earned credibility.